Politicians often have a narrative that is, shall we say, inconsistent with reality. Especially on economic matters. Joe Biden repeatedly told us that there was no inflation. And then that it was transient. And then he had defeated it, much better than all the other countries! See it was a global phenomenon, nothing to see here with my spending binge!* Mr. Biden called his disastrous, shameful Afghanistan retreat a “success” for the U.S., even while Americans grieved the unnecessary loss of 13 lives and had images of Afghanis clutching at the C17 as we cut and run. And then there were the almost daily lies about Mr. Biden’s mental acuity and energy, with Karine Jean-Pierre saying “I can’t keep up with him.” But trying to claim politically as truth what reality denies has costs, both to the country and the politicians. For Mr. Biden, Milton Friedman had his day when inflation went north of 9%, crashing the official narrative. For Mr. Trump, the analogous fiasco is his trade policy.** Just as Mr. Biden was steadfastly defiant with his Afghanistan “success”, so too is Mr. Trump sticking with his trade policy, independent of all the results (and once again being smacked down as illegal). Yet markets don’t care about political spin; markets are one of the few sources of truth*** in a narrative driven world.

Last Friday we had an utter debacle in the bond market, with long bonds spiking sharply higher, with the 10 year treasury hitting over 4.6% and the 30 year cresting over 5%, highs not seen since the early 2000s.

We’ve all heard the story of the straw that broke the camel’s back, and that is apropos here. There is not one single thing that led to this result, even though the biggest driver is expected future inflation., yet that has several nuances that we need to think about. Last week’s CPI was over 7% annualized, and inflation for the last year was 3.8%. For sure energy prices were the primary driver, but food prices were also higher. And even inflation minus food and energy (as if we all don’t need food and energy to live!) was 2.8%, well north of the prior decade and the stated Fed goal of 2%. April’s reading of prices paid in the Purchasing Manager’s Index was the highest in four years, as energy costs are getting baked into production. This suggests we’re not going to have prices immediately fall, even if the Iran war ends tomorrow. Similarly the Producer Price Index rose 1.4% in April, with an overall 6% increase in the last year. The best estimates I’ve seen suggest the about .75% of the CPI is due to tariff-related goods inflation with ~90% passed on to U.S. consumers. Suffice it to say that the American consumer has been pummelled with higher prices for years. We had Covid and associated supply chain shocks, the Biden inflationary response, Russia’s invasion of Ukraine and spiking energy, Mr. Trump’s “Liberation Day”, and now the Iran war. Steve Cahillane, the CEO of Kraft Heinz said earlier this month that their sales reflect that “consumers are literally running out of money” at the end of the month.

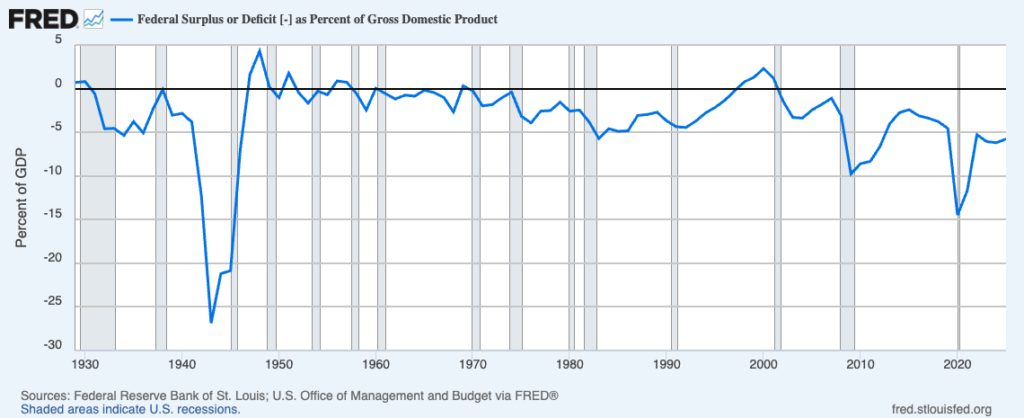

Yet 30 year bond yields shouldn’t spike dramatically for a short term increase in inflation; markets are pricing longer term inflation. And the reality is the bill is starting to come due of our collective refusal to deal with our addiction to spending in Western countries across the world. We recently crossed the line with 100% Debt to GDP rate, and are over $39T in debt with many more trillions in unfunded liabilities. The current administration has no serious plans to deal with it, as entitlements, which are the problem, are off limits. In other words, we know we’re in a hole, but we absolutely refuse to stop digging.

Our budget deficits since Covid are all over 5% of GDP and rising, with the projected situation getting worse. And we have no plans to deal with it. None. Mr. Trump’s plan? Get Kevin Warsh to go to the Fed and lower interest rates so we don’t have to pay for all this debt that I refuse to deal with. And now we have an Iran war and a proposed rapid increase in defense spending. Further, the one bright spot that is responsible for much of our GDP growth and business investment is AI infrastructure buildout, and the hyperscalers are now planning on borrowing a trillion dollars in the near term. This large increase in demand for capital means the government has to bid it away from the private sector.

So what are markets saying? You have no plan except inflation. And the inflation premium the bond vigilantes are putting in is on the rise. Last year we had the dollar debasement trade. Post this war, it is likely to be on the move again. I don’t see a pathway for interest rates to come down markedly; indeed the likely direction is now up not down, which is what the Fed rate futures are suggesting. Even worse, the average rate the U.S. is paying on it’s $39T in debt is less than the lowest rate we’re paying in T-bills, with 1/3 of the debt rolling over this year into higher rates. This means that our over $1T interest payments are going to go up, not down. The only silver lining is that debt is now so big and so meaningful in terms of interest that I believe it will quickly have to be dealt with. I expect this will be the major topic of discussion by the time the 2028 presidential election arrives.

Adam Smith will have his day.

* Except yes the spending went up radically across the globe and the global central banks monetized it. Not surprising that other countries would be hit harder, especially in Europe thanks to their energy dependency on Russia.

** I’ll come back to this soon in another post; tariffs are not today’s primary focus. Suffice it to say for now that just as none of his claims justifying tariffs were true, so too none of the hoped for results have come through. We’ve had all the pain with none of the supposed gain. More later.

*** I say truth very loosely, as market pricing reflects the subjective valuations of millions of people from varying perspectives. To the extent the current market price is “wrong” in some sense, it creates the very profit opportunity to take the price closer to the truth. Market prices are in a sense the composite, public “truth” which every private actor has to engage with.

Bert Wheeler

Bert Wheeler

Jeff Haymond

Jeff Haymond

Marc Clauson

Marc Clauson

Mark Caleb Smith

Mark Caleb Smith

Tom Mach

Tom Mach