The headline is perhaps unfair to Mr. Biden; there is a lot of nuance we could and should consider to last week’s report on the the 1QTR gross domestic product initial release of -1.4%. As the BEA notes in its release:

In the first quarter, an increase in COVID-19 cases related to the Omicron variant resulted in continued restrictions and disruptions in the operations of establishments in some parts of the country. Government assistance payments in the form of forgivable loans to businesses, grants to state and local governments, and social benefits to households all decreased as provisions of several federal programs expired or tapered off. The full economic effects of the COVID-19 pandemic cannot be quantified in the GDP estimate for the first quarter because the impacts are generally embedded in source data and cannot be separately identified.

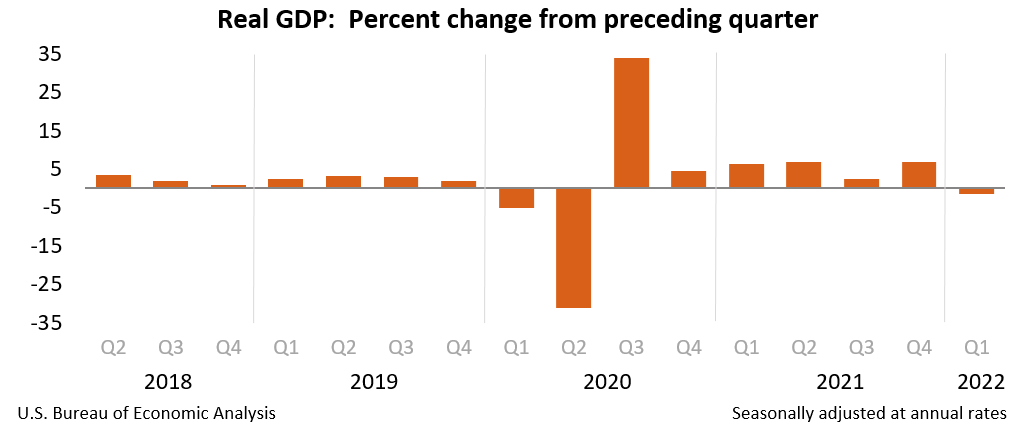

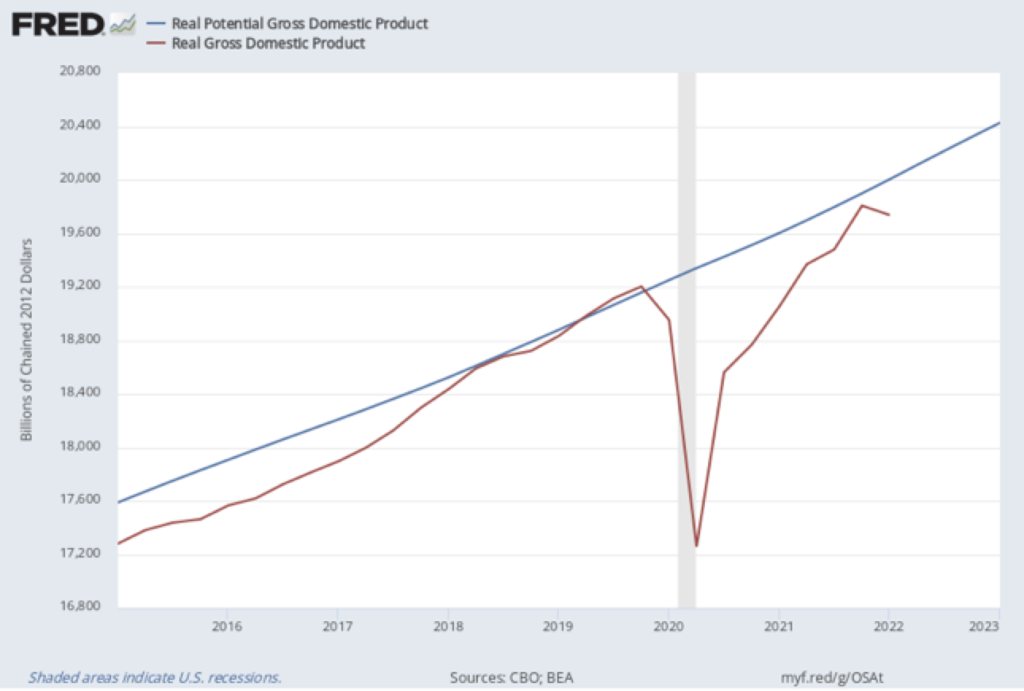

Yet there is at least as much reason to blame Mr. Biden for this low number (he’s been fully in charge for over a year, his party controls the congress and the executive department, if Covid is to blame–well, Mr. Biden promised he would end it in a few months, etc.) as for his ridiculous claims of the great economy we have under him during his first year. His claims of great GDP growth (true–as seen in the data above) were all based on the low comparables of the previous year. That’s a very flawed approach, as this simple illustration will show. Let’s say your $100k portfolio loses 50% of its value in one period, and then gains 75% the next period. Joe Biden’s logic is that you should be really happy with that result. Yet your former $100k portfolio is now worth only $87.5k, because the 75% gain was on the much lower number. You can see that even in the numbers above with the big Q2 spike down in 2020 and compared to the even larger spike up in Q3–but we all know that the economy wasn’t completely recovered by the start of the 4th Quarter of 2020. That’s why we see the very large growth numbers throughout 2021, as more and more shut down resources began to be employed. A better way to look at it would be a comparison of GDP to potential GDP (which estimates what GDP would be with full utilization of resources):

As you can see, under the Trump economy pre-covid we had caught up all the slow Obama years and were “running hot” while now under the Biden administration we have almost got back to where we were, but Q1 is starting to take us in the other direction. Mr. Biden’s claims of the great recovery he was engineering (which was really an artifact of people going back to work) is the proverbial rooster crowing and taking credit for the sunrise. With the easy comparables from the pandemic year now in the rear-view mirror, we’ll see the results of Biden economy each quarter.

But we don’t have to see the future GDP numbers to know that the Biden administration is killing us; Mr. Biden’s laugh at the correspondent’s dinner last week will be turning to tears in November:

Inflation continues to eat away at our salaries; compare the Trump years earnings growth to Mr. Biden’s. If the recovery is so strong, why are real wages declining so rapidly?

The Biden Administration does have some negative headwinds that make all these numbers worse–yes the supply chain issues are real, even if supply chain issues NEVER lead to inflation*. And Russia is a real negative to the economy.** Production processes are already being reordered across the globe, and not just Russia–you’re going to see an acceleration of the trend for companies to look for alternatives to China. Free trade really does make the world richer materially–we’re getting ready to create new production processes that are necessarily less efficient than what we were doing (or we wouldn’t have waited until now to do them!), and that’s going to continue to make the world a bit poorer. The Biden Administration’s stubborn refusal to unleash American energy production will make us poorer, and geopolitically far weaker.

It is not too early to declare this a failed presidency. I could have hope, but Mr. Biden makes every wrong move and has steadfastly refused to pivot. November is a coming.

* Supply chain issues can lead to a higher price level, but not an ongoing inflation–inflation is always a demand side of the economy phenomenon. In the presence of a negative supply shock, like Covid, you would expect to see prices rise for those goods/services that see supply disrupted, and with a stable monetary policy that did not “accommodate” the inflation, other goods and services’ prices would necessarily fall. It is the printing of money in response to supply-side issues that leads to inflation. And as we’ve discussed repeatedly, the Fed printed $5T in new money to buy up all the government debt added during the pandemic period.

** But it is an open question in my mind whether Russia would have invaded Ukraine if we didn’t have a weak administration that 1) shamelessly retreated in Afghanistan (and then crowed about it!), and 2) did nothing when the Russians massed 70k troops on the Ukrainian border. It’s possible that they would have invaded in a Trump II administration, but the Biden Administration’s weakness made it a more open invitation (remember we’ll tolerate a minor incursion).

Bert Wheeler

Bert Wheeler

Jeff Haymond

Jeff Haymond

Marc Clauson

Marc Clauson

Mark Caleb Smith

Mark Caleb Smith

Tom Mach

Tom Mach